As of today, the dollar rate in Nigeria stands at almost 1500 Naira to a dollar. This fluctuation has reverberated throughout the Nigerian economy, casting a shadow of uncertainty and hardship over businesses and households alike. The ripple effects of this exchange rate volatility have been felt across various sectors, from import-dependent industries struggling with rising costs to ordinary citizens grappling with the erosion of their purchasing power.

Nigerians, feeling the pinch of this economic turmoil, are increasingly vocal in their calls for government intervention. As inflationary pressures mount and the cost of living continues to soar, there’s a palpable sense of urgency for decisive action to be taken. The people are crying out to the government, demanding solutions to alleviate their financial burdens and steer the nation towards stability and prosperity.

Is the Dollar Rate Behind Nigeria’s Economic Crisis?

In July 2023, the Nigerian President, Bola Ahmed Tinubu declared an urgent State of Emergency on food insecurity in response to the escalating global issue of rising food prices. He directed that “all matters related to food and water availability and affordability, recognized as essential elements for livelihoods, be addressed within the scope of the National Security Council.”

Possibly, the President’s decision was prompted by the cries of Nigerians, exacerbated by his government’s removal of subsidies on premium motor spirit, commonly known as petrol, on May 29, 2023. However, the current situation is cause for deep concern. Since the subsidy removal, virtually every commodity in the country has experienced a more than twofold increase in prices, rendering essential items, particularly food, inaccessible to the economically disadvantaged. Even the affluent are facing hardships.

In the year 2024, the relentless surge in food prices persists and is expected to escalate further as the year unfolds. The Consumer Price Index (CPI), a measure of the rate of change in prices of goods and services, reached 28.92 percent in December 2023, up from 28.20 percent in the previous month, as reported by the National Bureau of Statistics (NBS) in its December CPI report.

From basic items such as sachet water, affordable noodles, to staples like ‘garri,’ people now find themselves paying more for diminished quantities of these necessities.

Who Do We Blame?

Editor’s Choice

What lies at the heart of this profound economic downturn in Nigeria? A recent in-depth investigation conducted by the StartupsVibes Team sheds light on a prevailing sentiment among Nigerians, pointing fingers at the devaluation of the Naira against the dollar. The majority of citizens place blame squarely on the government and the Central Bank of Nigeria (CBN) for the dire state of the economy, the surge in prices, and the exorbitant cost of living. Yet, the crucial question remains: Is the Dollar Rate the Sole Culprit Behind Nigeria’s Unfolding Economic Crisis?

The complexities of a nation’s economic challenges are seldom reducible to a single factor, and Nigeria is no exception. While the depreciation of the Naira plays a pivotal role in the economic landscape, it is essential to explore a multitude of interconnected issues contributing to the current predicament.

One notable factor is the global economic dynamics and geopolitical shifts affecting commodity prices, particularly oil – a cornerstone of Nigeria’s economy. As a major oil exporter, Nigeria’s fortunes are intricately tied to the fluctuations in global oil prices. Any adverse movement in this realm can have cascading effects on the nation’s fiscal health and the purchasing power of its citizens.

Moreover, systemic issues such as corruption, mismanagement of resources, and infrastructural inadequacies persistently hinder Nigeria’s economic resilience. The lack of effective policy measures to diversify the economy away from its heavy reliance on oil exacerbates vulnerabilities in the face of external shocks.

The StartupsVibes Market Survey

Editor’s Choice

In a recent market survey conducted by the StartupsVibes Team, a nuanced narrative emerged, diverging from the prevailing discourse centered on the dollar’s blame game. Delving into the vibrant local bazaars, our survey uncovered the candid perspectives of market sellers, providing valuable insights into the factors fueling the relentless rise in commodity prices.

The survey video captured the voices of a meat vendor and a vegetable seller, who unveiled the intricacies of their daily struggles intricately tied to the elevated costs of transporting livestock and vegetables from farms to bustling markets. These localized challenges, often overshadowed by macroeconomic discussions, lay bare the grassroots realities that shape market dynamics.

A poignant portrayal of the current plight unfolded through the lens of a food seller, articulating the collective despair of Nigerians unable to savor the simple joy of a hearty meal. The rising cost of sustenance and diminishing food portions have reshaped the culinary landscape, turning the once-commonplace act of dining out into an elusive luxury for many.

Within the frozen delights section, our survey uncovered a seller attributing the surge in prices of Turkey, Chicken, and Fish to the intricate dance of currencies. With Nigerians heavily reliant on importing 90% of their frozen goods from Cotonou, the ripple effects of the Naira’s depreciation against the Dollar reverberate, transforming once-affordable items like Titus fish into symbols of privilege.

Adding a theatrical flair to the findings, a bottled water seller passionately underscored the burdensome nature of the cost of living. Her fervent emphasis shed light on the uphill battle faced by many in meeting rent payments, sparking a plea for a reduction in the price of cement—a call resonating beyond the aisles of water bottles, echoing the broader desire to alleviate the heavy financial burdens faced by a significant portion of the population.

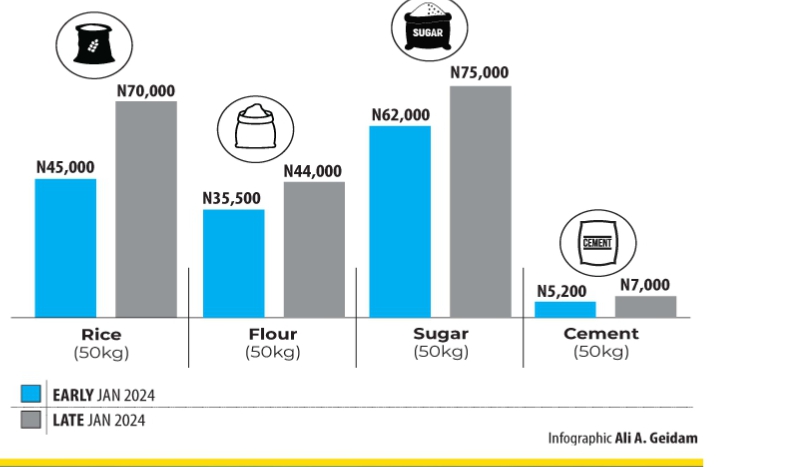

Still on our survey conducted at the Corner Market in Lagos, Nigeria, StartupsVibes observed noteworthy trends in the pricing of essential commodities, shedding light on the challenges faced by both sellers and consumers.

A stark reality emerged as a 50kg bag of foreign rice commanded a price range of N65,000 to N70,000, while local rice stood at N65,000. Meanwhile, at Iponri Market, 10kg of Semovita was priced at N11,500, and a paint bucket of beans fetched N13,500. The survey also revealed that a bag of sugar now comes with a hefty price tag of N63,000.

What is particularly concerning is that these price dynamics seem to hold steady across various regions of the country. In the Corner Market, Mrs. Ireti Olorunsogo, a restaurant owner, expressed her distress over dwindling customer patronage due to the soaring prices of commodities and the diminished purchasing power of citizens nationwide.

“Everything has gone high,” she lamented. “Maggi moved from N700 to N1,200 per pack, and Spaghetti is N750 to N800 depending on the brand. We are not making any gain; we are just struggling to feed the family. The money will go towards buying things (family’s essentials).”

In response to the economic challenges, Mrs. Olorunsogo disclosed that she has been compelled to reduce the quantity of food she serves to customers. She called on the government to intervene, emphasizing the need to address the plight of the people.

“Instead of increasing the price again, we reduce the quantity. People are not eating to get satisfied. I don’t have many customers like before. A plate of food I was selling for N300 is now N800.”

She urged the government to consider measures such as opening borders to make imported goods more accessible and affordable, citing the inadequacy of local production to meet the demands.

Adding a voice to the chorus of concerns, an apprentice, Oyekan Opeyemi, shared his perspective on the challenging economic climate in Nigeria.

“Nigeria has become something else. If I have my way to get out of this country, I will not come back again. The country is full of stress. The government has failed the people,” he expressed, highlighting the increasing difficulty of survival as the cost of living rises while workers contend with inadequately low wages from both government and private organizations.

How Can We Fix Nigeria?

The Nigerian government holds a crucial responsibility in addressing the economic distress gripping the nation. It must implement comprehensive policies and strategies to stimulate economic growth, reduce poverty, and promote social equity. Key initiatives may include:

- Infrastructure Development: Investing in infrastructure projects to bolster economic activity and create job opportunities.

- Economic Diversification: Expanding beyond oil dependency by investing in sectors such as agriculture, manufacturing, and technology.

- Social Safety Nets: Establishing robust social welfare programs to provide assistance to vulnerable citizens and mitigate the impact of economic hardships.

Private Sector Engagement: A Collaborative Approach

We believe that, beyond government intervention, collaboration with the private sector is essential to address Nigeria’s economic challenges effectively. Successful business leaders and entrepreneurs can contribute to job creation and economic development through investments and innovative ventures. Encouraging private sector involvement in social causes and philanthropy can also make a significant difference in supporting communities in need.

Join us in the movement for a thriving Nigeria!

Are you passionate about seeing Nigeria rise above its current economic challenges and achieve a prosperous future? We want to hear from you! Share your insights on how Nigeria can build a robust economy and uplift its people from poverty and suffering.

Imagine a Nigeria where every citizen has access to opportunities, where economic growth is inclusive, and where poverty is a thing of the past. This vision is within reach, but it requires collective action and innovative solutions.

The government has a crucial role to play in this journey. By implementing sound economic policies, investing in infrastructure, and fostering an enabling environment for businesses to thrive, the government can pave the way for sustainable growth and development. Additionally, promoting transparency, accountability, and good governance is essential in rebuilding trust and confidence in our institutions.

But it’s not just up to the government. Each one of us has a part to play in shaping Nigeria’s future. Whether you’re an entrepreneur, a professional, or a concerned citizen, your contributions matter. By supporting local businesses, investing in education and skills development, and advocating for social justice and equality, we can collectively drive positive change in our society.

Share your thoughts in the comment section and join us in the Startups Forum, where passionate individuals and professionals come together to dissect and discuss pertinent issues affecting our ecosystem. Together, let’s brainstorm ideas, share best practices, and collaborate on initiatives that will propel Nigeria towards a brighter and more prosperous tomorrow.

Together, let’s build a better Nigeria. Join the movement today!